Buxy

White label Fintech super-app

2 week sprint

April 2024

The Problem

Millions of people use traditional banks, but they are slow to adapt. With Buxy, they will be able to compete with challenger banks. The goal is to generate revenue from banks and help maximize their opportunities to serve their customers.

The Challenge

Our objective was to transform banking services by developing a plug-and-play solution for traditional banks, offering users a super-app experience. The aim is to support traditional banks in boosting revenue, adapting swiftly, and competing effectively with challenger banks, thereby enhancing customer service opportunities.

Key success metrics include reaching a product stage where stakeholders can apply for a fintech incubation program, with the ultimate goal of securing additional investment.

Create a revolutionised banking service by developing a plug-and-play solution for traditional banks that brings a super-app experience to their users. This will be achieved through personalised lifestyle content, a marketplace, bonuses, and education offers.

Key insights from stakeholder interview

Lifestyle

Marketplace

Education

Competitor analysis

After our stakeholder interview we looked into a variety of competitors. These ranged from the direct competitors, in this case, the challenger banks like Revolut and Monzo and also a large selection of other apps that are known for having highly praised features, for example Spotify’s personalization.

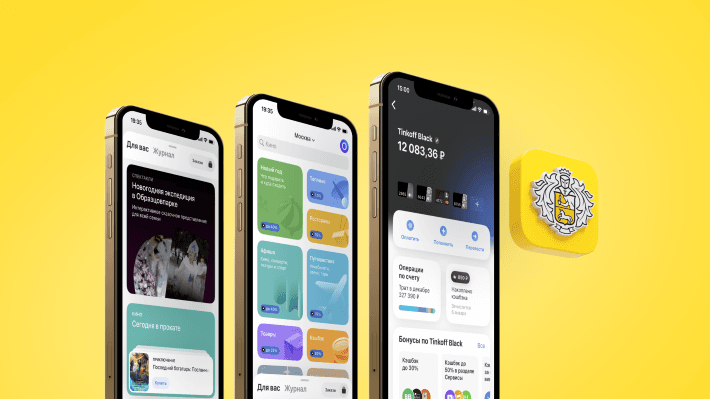

Tinkoff

We also researched the Tinkoff bank ‘super app’ as a source of inspiration for the Buxy concept. It’s praised for it’s vast reach in gamification which boosts user engagement with it’s app.

Revolut

Revolut was a key competitor as it is the most popular challenger bank that rivals traditional banks on a technological and user friendly way. We discovered a clear opportunity for Buxy as these challenger banks lack many traditional features such as mortgages/personal loans and the inability to deposit cash or cheques.

Spotify

More of an indirect competitor - Spotify is widely known for having exceptional personalisation with the constant updates and push for Daily/Weekly mixes and playlists, tailored podcasts and a huge discovery library.

Desk research, Qualitative and quantative data

Conducting general research provided us with a deeper understanding of the fintech landscape, particularly focusing on challenger banks and their impact.

We surveyed millennials between the ages of 28 – 43 and gathered data from 82 respondents.

We undertook 20 user interviews and gathered over 80 data points.

Key insights from research

Engagement

Rewards

Users had a generally positive experience with rewards but showed scepticism around hidden catches or costs, which can then lead to mistrust. Users currently mainly use rewards through Unidays and American Express.

Personalisation

It was clear that users desire more personalisation as whilst their current platforms have this to some degree, they’d like to be able to customise features more. Many showed a preference for detailed personal financial planning tools.

74% of users currently use some form of traditional banks.

Rewards were offered by 46% of users banks, yet of those offering these 60% rated the rewards available to them negatively.

Affinity mapping

Affinity mapping helped us to organise our research data from user interviews into meaningful categories to identify patterns and insights.

We grouped our interview research into ‘security and privacy’, ‘research and marketplace’, ‘engagement with banking app’ and ‘discovering new features’.

Here are common themes we found.

Key insights from research

Security & privacy

Essential for user trust; clear communication about data protection is crucial.

Traditional banks are trusted more; newer banks need transparency and strong security to build trust.

Rewards & marketplace

Rewards programs need to be transparent to build trust. Clear instructions on how to redeem rewards are crucial.

Simplifying the process of earning and redeeming rewards will encourage more users to participate.

Engagement with banking app

Users engage with their banking apps regularly, typically 1-3 times a week.

Users prefer all-in-one apps that include money management, budgeting tools, and comprehensive analytics.

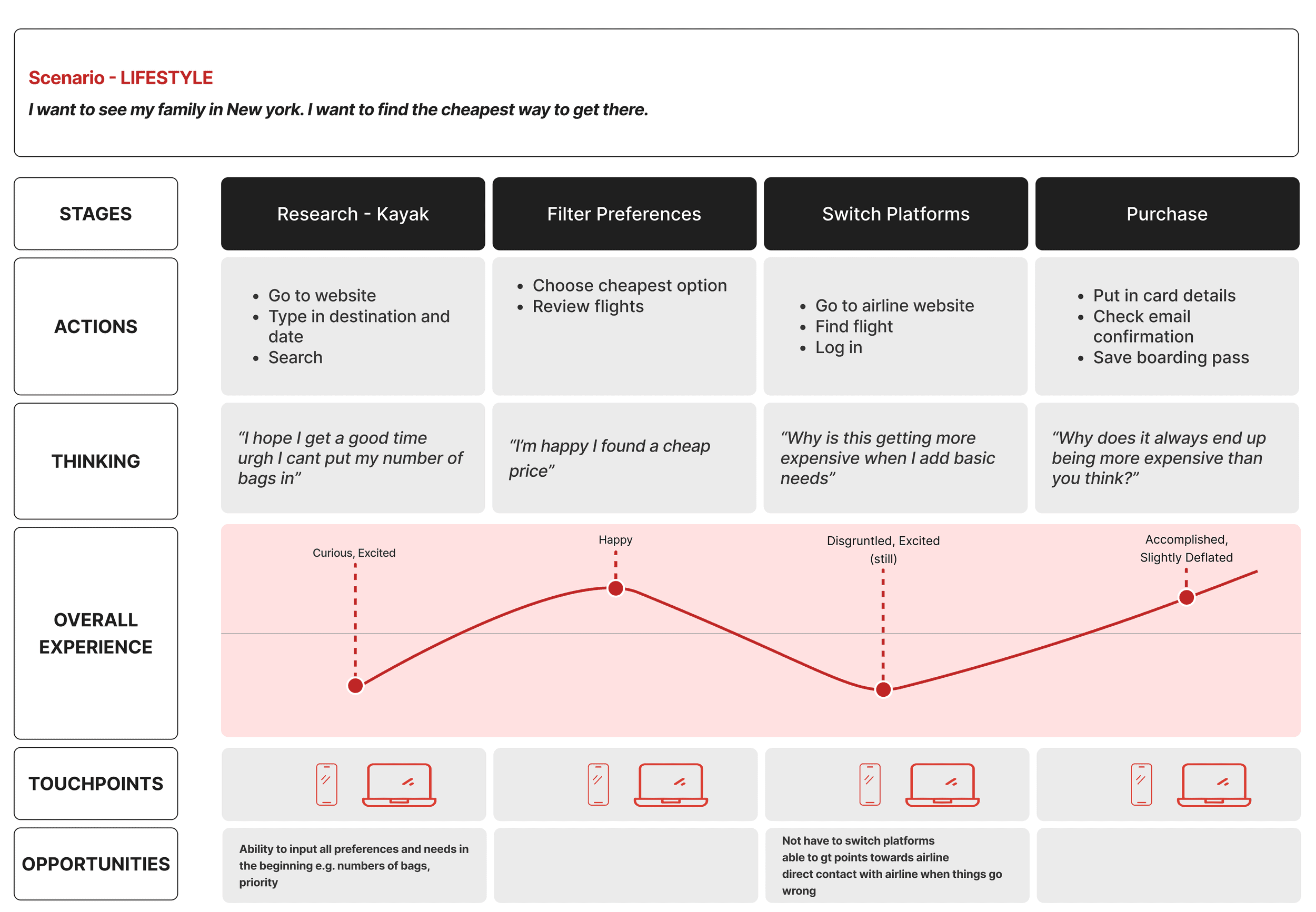

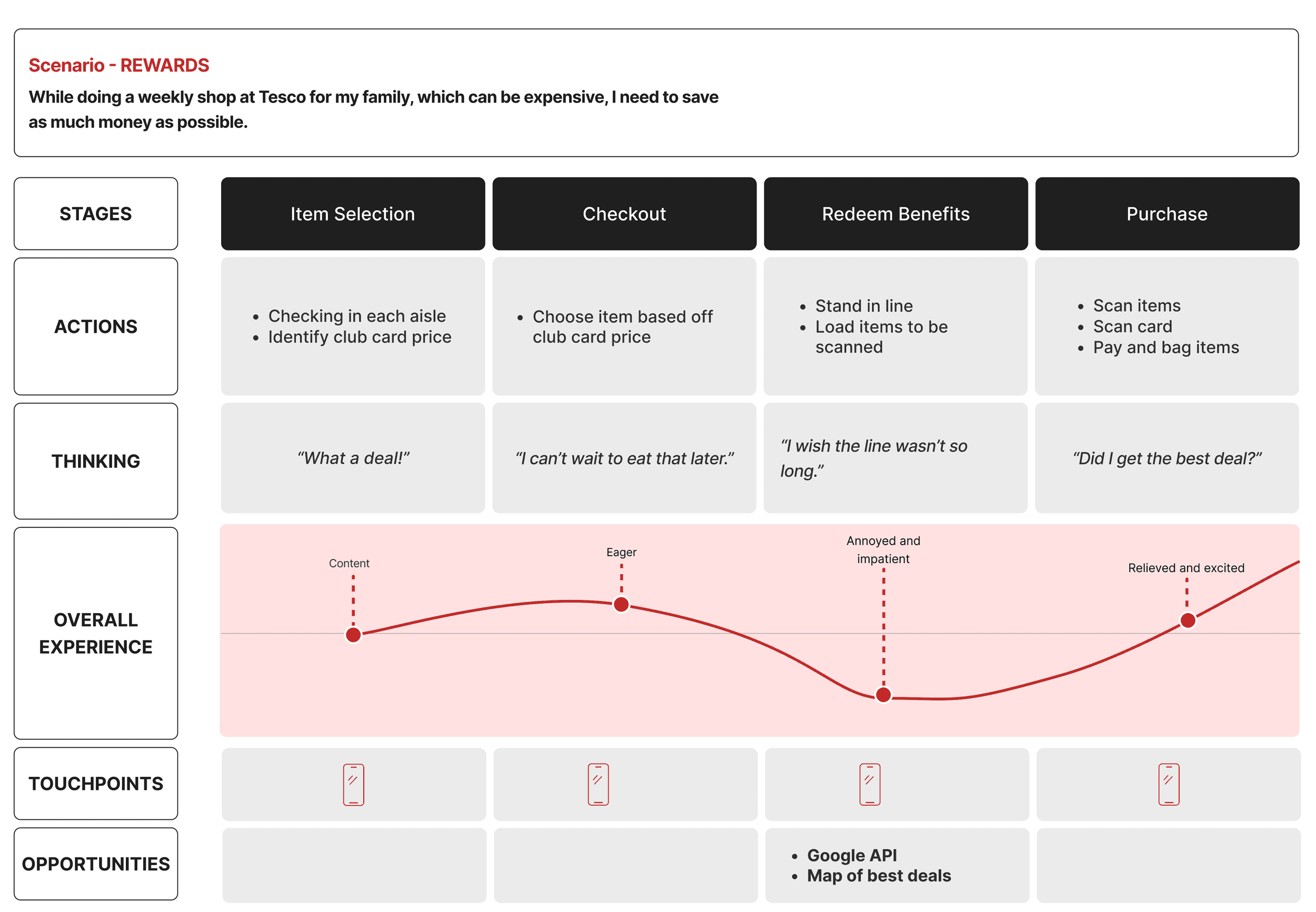

Experience maps

We continued on to experience mapping to visualise the user’s journey through current experiences to highlight pain points and opportunities for improvement in financial transactions and finding the best deals.

Key pain points users currently experiences area lack of transparency in saving opportunities, information overload and frustration finding the right offers, as well as lack of customer loyalty benefits.

Problem statements

We continued on to experience mapping to visualise the user’s journey through current experiences to highlight pain points and opportunities for improvement in financial transactions and finding the best deals.

Key pain points users currently experiences area lack of transparency in saving opportunities, information overload and frustration finding the right offers, as well as lack of customer loyalty benefits.

Defining how Buxy can deliver value to its's users

We live in a consumer oriented world. We often spend money but don’t know how efficiently we are spending it.

There are opportunities to save money or to be rewarded, however we are often unaware of where to look and how to maximise our savings.

Traditional banks have huge usership and there is a large opportunity to further enhance value that current consumers get.

Buxy’s plug and play solution can deliver huge value, not only to traditional banks, but also to millions of end users.

Value proposition canvas

I went on to create some VPCs which are essentially a visual tool that maps out the customer profile and the value proposition, allowing me as a designer to identify potential pain points and areas where their product can create value. These are the scenarios I focused on.

When I am shopping around for a mortgage I would like to be aware of the quality of the products and services available to me so that I get the best deal.

Pains: Mortgage jargon is confusing, overwhelmed with options, time consuming, worried about making a mistake. Very costly, boring subject.

Gains: Less financial stress each month, more money to spend on lifestyle, feeling comfortable with my decision, feeling informed.

Jobs to be done: Secure optimal mortgage deal, get on the housing ladder, save Money.

Pain relievers: Clear and easy UI so users can access educational content quickly, Bite sized lessons that are easily digestable,

Gain relievers: Test / quiz to give you CLEAR personal advice.

Products and services: Gamified quiz to learn more about mortgages.

When I use my banking app, I want to receive personalised tips / insights about missed opportunities so that I can save money in the future.

Pains: Not feeling informed, Financial stress, overwhelmed with the volume of banking tips available online.

Gains: User confidence, more cash to spend on lifestyle,fFind more and better deals available to them, more awareness of spending habits, improve financial decisions moving forward.

Jobs to be done: Unlocking financial literacy, find easier to digest financial information, Find trusted tips / insights.

Pain relievers: High quality content that genuinely informs users, ‘Heres how much you saved with Buxy’ element to ease stress / make benefits clear, Streamlined selection of personalised tips that live inside and are endorsed your trusted bank’s app.

Gain relievers: Personalised tips / insights based on your bank statement.

Products and services: Bank statement assessment tool that identifies missed saving opportunities / habits.

Jobs to be done framework

"Jobs to be Done" is a framework to help us identify the functional, emotional, and social tasks that users aim to accomplish with the product. Depending on the project, this process is often an effective alternative to generating ‘personas’ as it focuses on the specific tasks users are looking to achieve.

For the Buxy project we broke this down into ‘lifestyle’, ‘rewards’, ‘education’ and ‘personalisation’.

Here are some key jobs to be done that I decided to focus on for my MVP build.

When I use my banking app, I want to receive personalised tips about missed opportunities so that I can save money in the future.

When I buy new shoes, I want to find the best deal, so I can save money.

When I use my banking app, I want to receive personalised tips about missed opportunities so that I can save money in the future.

Rapid ideation & crazy 8s

With a clearer idea as to what jobs Buxy users might be looking to get done, we started the develop phase with rapid ideation sessions using a technique called crazy 8s.

This is where we split off and further developed our own individual problem statements and ideas. I decided that I wanted to design for all three core use cases - lifestyle, education and personalisation.

Low fidelity wireframes

After hand-sketching and fleshing out all three of my wireframe flows it was time to jump into Figma to develop them further. The goal was to get to a point where I could start connecting the frames together as a prototype in order to carry out in-person user testing.

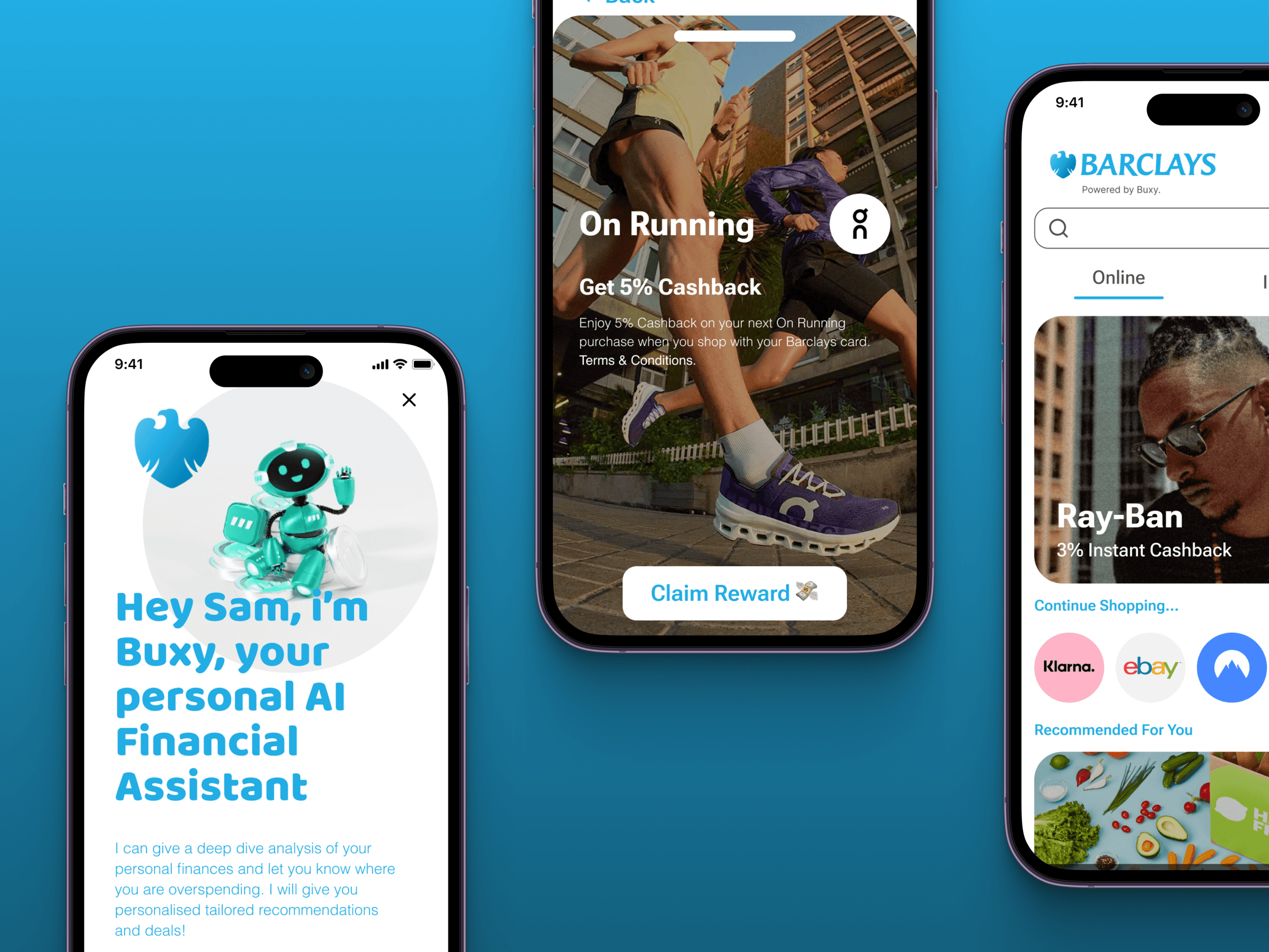

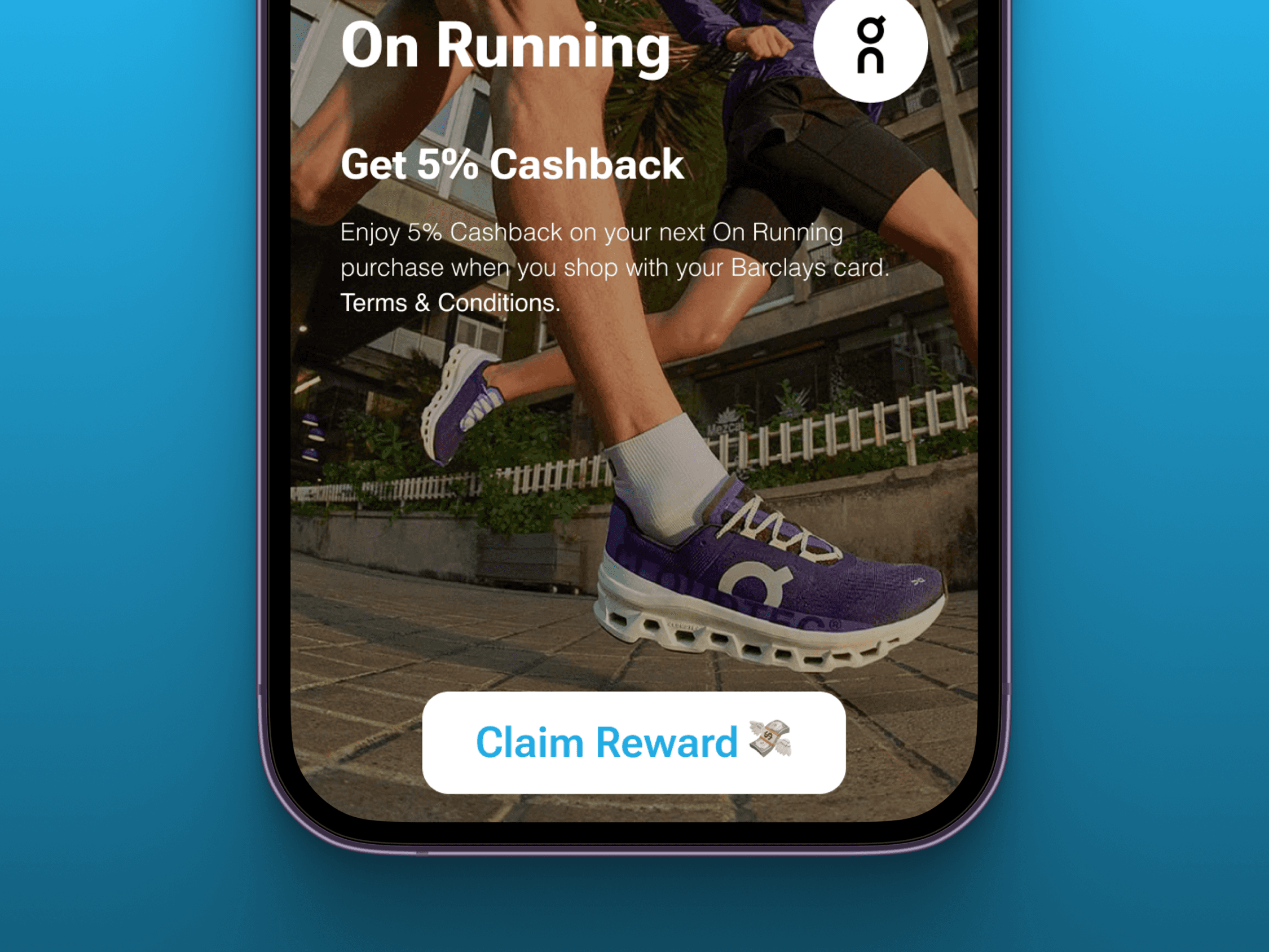

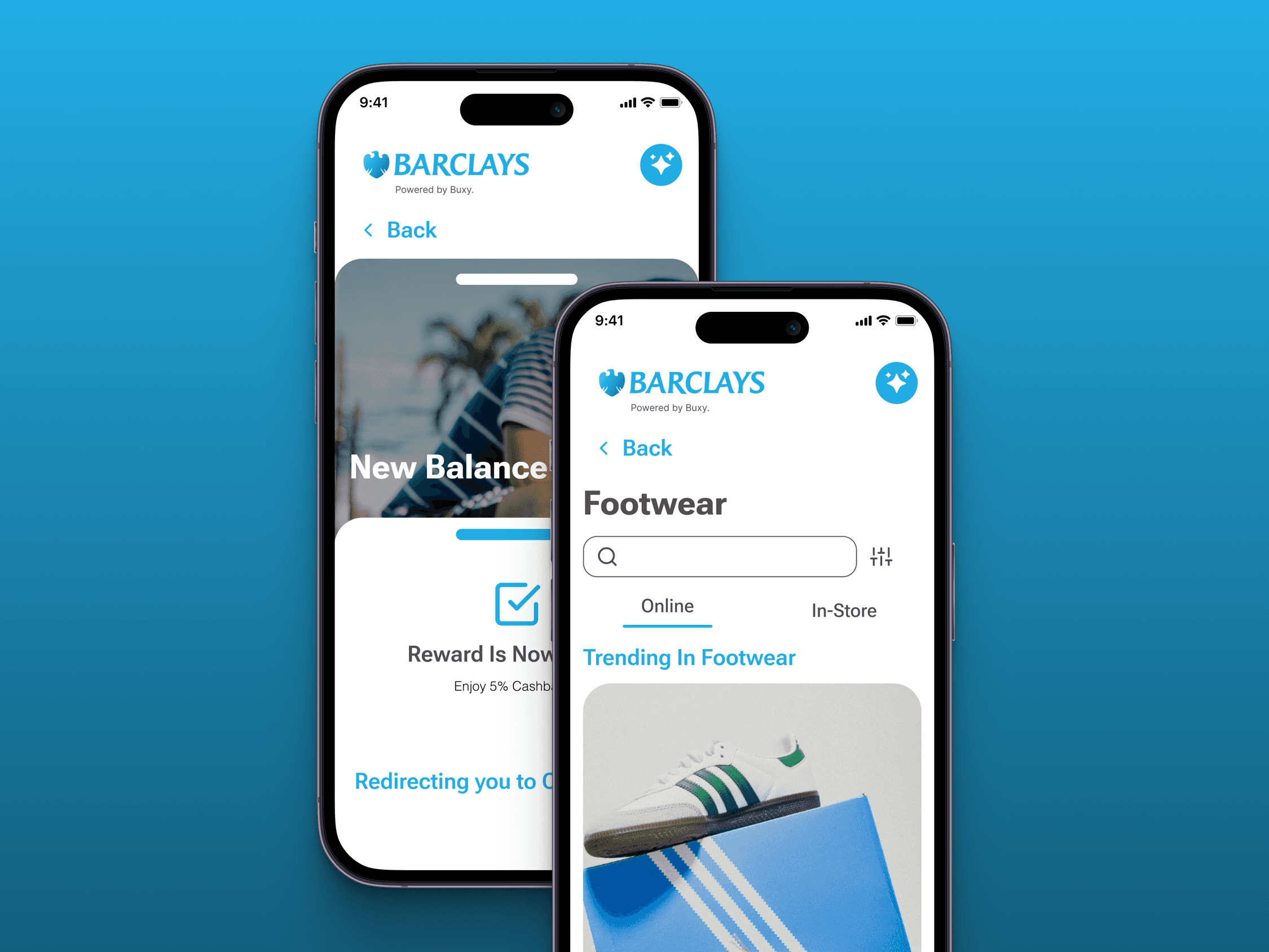

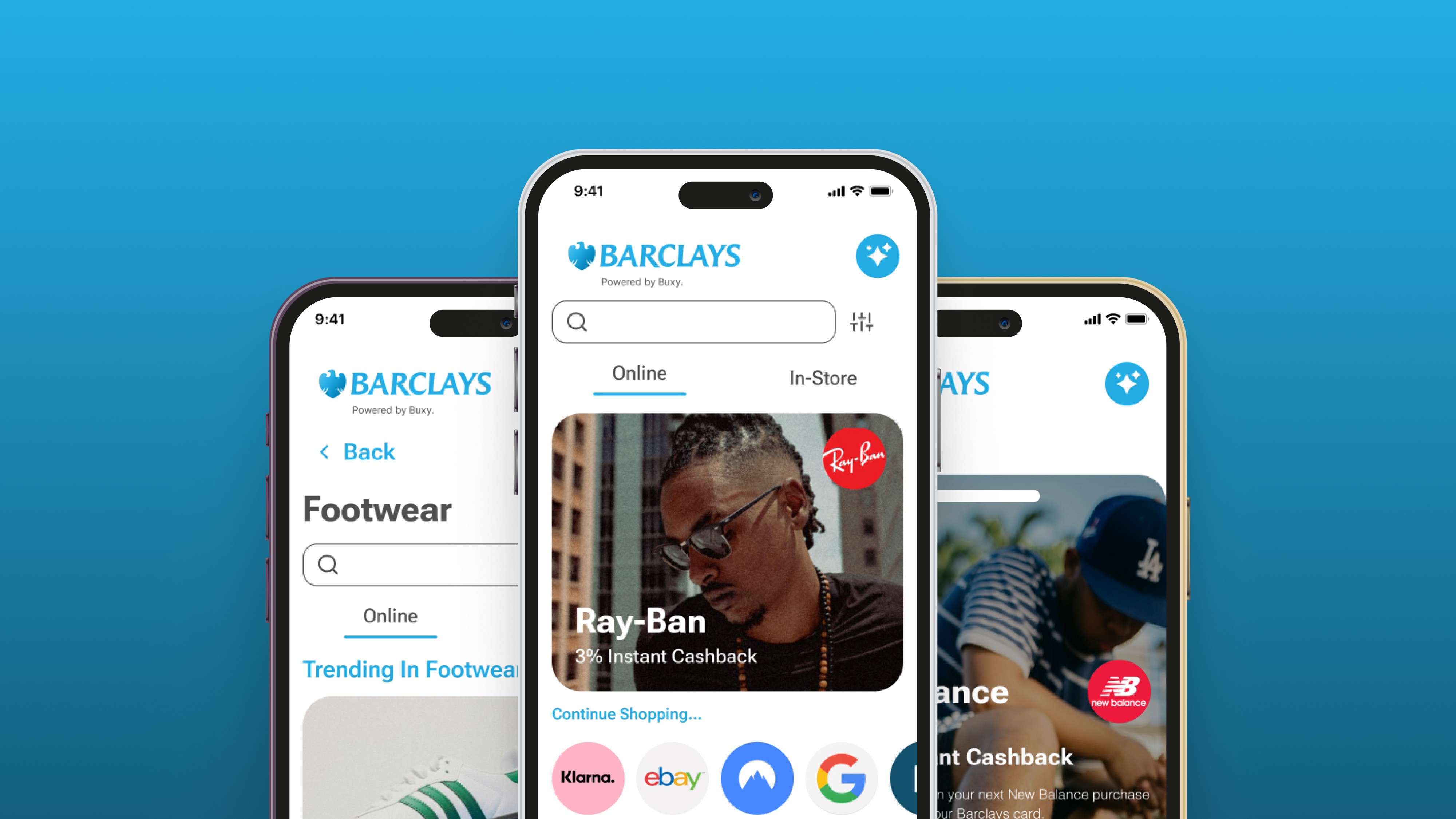

Final High fidelity wireframes

Once I was happy with my three flows and the concept behind each screen it was time to move onto the high-fidelity prototypes that I would be presenting to the client.

I took inspiration from the design language of challenger banks like Monzo and Revolut. These banks are leading design in the Fintech sector.

Playback to Buxy team

To round up our 2-week Fintech design sprint we presented our work to Buxy founder Stanislav at Experience Haus, Shoreditch. He was really impressed with the deliverables we were able to produce in such a short time.

Post the successful final presentation itself the final step was to neatly package up all the relevant files and deliverables for the stakeholder.

Our work over the two weeks will play a big role in this start up getting further investment and funding.